Businesses today can’t afford to ignore digital payments. Whether you sell online or offline, your customers expect a quick, convenient way to pay. But setting up these payment options isn’t always simple. Behind every smooth transaction is a system that connects your business to your customer’s bank—and that’s where a payment service provider (PSP) comes in.

Understanding how a PSP works can help you offer more payment choices, speed up settlements, and avoid common payment issues. This article breaks it down clearly, so you know what to look for when choosing one for your business.

What is a Payment Service Provider?

A payment service provider is a third-party entity that helps businesses accept payments from customers through various digital methods. This includes debit and credit cards, UPI, net banking, digital wallets, and sometimes even Buy Now Pay Later (BNPL) options.

Instead of building your own system to handle each of these methods separately, you can use a PSP to manage everything in one place. It acts as the link between your business, your customer’s bank, and your own bank account.

In simple terms, a PSP makes it possible for you to collect money from customers through digital channels and ensures that it reaches your account safely and efficiently.

What Does a PSP Do?

A PSP handles several key parts of the digital payment process. Here’s what that looks like:

1. Payment Processing

When a customer makes a payment, the PSP processes the transaction in real-time. It checks if the payment method is valid, confirms with the customer’s bank, and facilitates the transfer of funds to your account.

2. Multi-Channel Support

Most PSPs offer a range of payment options—card payments, UPI, wallets, QR codes, EMI options, and even recurring billing. This flexibility makes it easier for businesses to serve a wider customer base.

3. Security and Compliance

A reliable payment service provider ensures that all transactions are encrypted and secure. PSPs are expected to follow the regulations laid down by the central bank and other authorities, including data protection and anti-fraud measures.

4. Settlement and Reconciliation

After a successful payment, the PSP initiates settlement to your linked bank account—typically within 1 to 3 business days, depending on the payment method and provider. Some PSPs also offer instant or same-day settlements for an additional fee. They provide dashboards or reports to help you reconcile transactions, monitor settlement status, and manage refunds or disputes.

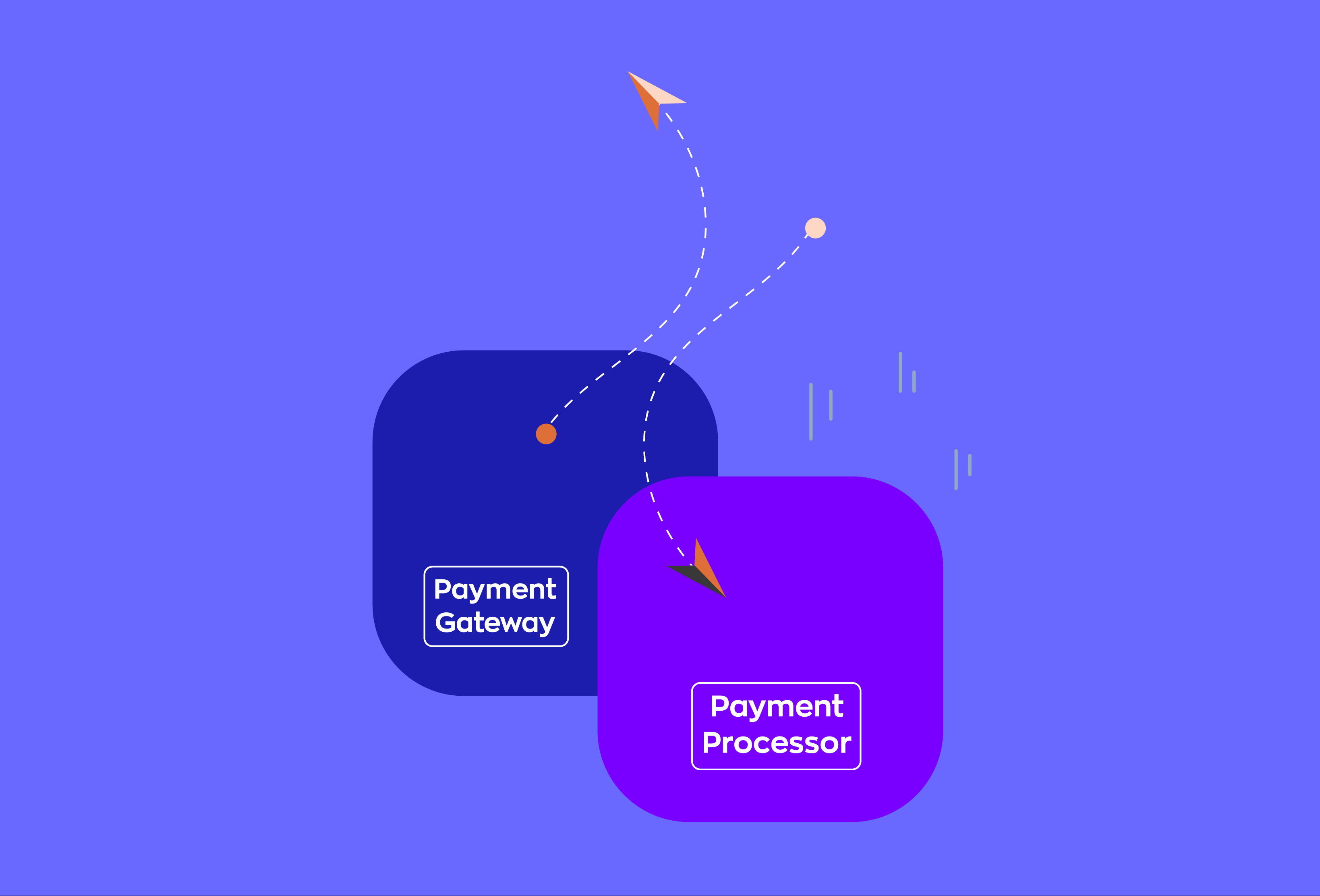

Is a PSP the Same as a Payment Gateway?

Not exactly. A payment gateway is the technology that captures and sends card details or UPI requests to the banks. It’s part of the payment flow but not the complete solution.

A payment service provider, on the other hand, offers an end-to-end solution. It may include the payment gateway, but also handles settlements, risk checks, compliance, and customer support. Many companies offer both services together, which is why the two terms are often used interchangeably, but they are not the same.

If you’re setting up a digital payment system for your business, a PSP will typically be the more complete option.

Why Do Businesses Use a Payment Service Provider?

There are several benefits to using a PSP, especially for businesses looking to grow and scale:

1. Faster Setup

Integrating with a PSP is usually quick and doesn’t require major technical effort. Many providers offer plug-and-play options for websites, mobile apps, and even offline stores.

2. Increased Customer Convenience

Offering multiple payment options improves the chances of a successful sale. If a customer prefers UPI over cards or wants to use a wallet, the PSP makes that possible without you having to manage each method individually.

3. Reliable Settlement

Most PSPs ensure timely settlement—often within 1 to 3 business days—though timelines can vary based on your business profile and payment method.

4. Fraud Protection and Security

Payment service providers monitor transactions for suspicious activity. This helps protect your business from fraud and ensures that you stay compliant with payment regulations.

5. Customer Support

When payment failures happen—or if a customer has been charged twice—it’s important to resolve the issue quickly. Most PSPs have support systems in place to handle such queries efficiently.

How to Choose the Right PSP for Your Business

Not all PSPs are the same. Choosing the right one depends on your business needs, transaction volume, and the kind of customer experience you want to offer. Here are a few things to keep in mind:

1. Payment Options

Check if the PSP supports the payment methods your customers prefer—cards, UPI, wallets, net banking, etc.

2. Settlement Time

Understand how long it takes for payments to reach your account. Some PSPs offer daily settlements; others may have a fixed schedule or on-demand options.

3. Pricing and Fees

Look at the cost structure. This may include setup fees, transaction charges (also called MDR or merchant discount rate), and charges for refunds or chargebacks.

4. Ease of Integration

If you’re building a website or app, your development team will need to integrate the PSP’s APIs. A well-documented system with clear support can save time.

5. Dashboard and Analytics

Having access to a clean, easy-to-use dashboard helps in tracking transactions, identifying failed payments, and resolving disputes.

6. Security and Compliance

Check for PCI DSS compliance, especially if you’re accepting card payments—it’s essential for securely handling sensitive cardholder data. Also look for encryption standards and fraud prevention tools like tokenization, 3DS, or velocity checks.

7. Customer Support

Check if the PSP offers prompt support, especially during high-volume days like festive seasons or sales campaign. Also, in markets like India, PSPs operating UPI or wallet-based models must be authorised by the RBI. Choosing a PSP with the right licenses ensures regulatory compliance and business continuity.

Final Thoughts

A good payment service provider does more than just enable digital payments—it simplifies the entire process for businesses. From offering multiple payment options to ensuring that money reaches your account securely and on time, a PSP plays a vital role in keeping the business running smoothly.

Whether you’re a startup or an established company, choosing the right PSP is a key business decision. It impacts your customer experience, cash flow, and operational efficiency. Taking the time to understand how a PSP works—and what to look for—can go a long way in setting your business up for success.If you’re building your own payment infrastructure or embedded finance product, Zwitch offers developer-friendly APIs and no-code tools that give you the flexibility and control to design, integrate, and scale payment and banking experiences tailored to your business.