Opening a bank account, investing in mutual funds, or buying insurance often comes with the same frustrating step—submitting your KYC documents again and again. Identity proof, address proof, photographs—it’s repetitive, time-consuming, and easy to get wrong.

Central KYC (CKYC) was introduced to fix exactly this.

It allows you to complete your KYC once and reuse it across banks, NBFCs, mutual funds, and insurance providers in India. No more starting from scratch every time you access a new financial product.

In this guide, we’ll break down what CKYC is, how it works, how to register, and why it matters for faster, smoother financial onboarding.

Quick Summary

- CKYC stands for Central Know Your Customer

- It is a centralized KYC repository managed by CERSAI

- A single CKYC number can be used across banks, NBFCs, mutual funds, and insurance providers

- It reduces repetitive documentation and speeds up onboarding

What is CKYC?

CKYC stands for Central Know Your Customer. CKYC full form refers to Central Know Your Customer, a centralized KYC system in India. It is a centralized repository of KYC records of customers in the financial sector. Introduced by the Government of India, CKYC is managed by the Central Registry of Securitization Asset Reconstruction and Security Interest (CERSAI). The revamped CKYC registry announced in Union Budget 2025 signals a new era of convenience and compliance in India’s financial sector.

Here’s the essence: once your data is uploaded to the CKYC registry by any financial institution, your records become accessible (with proper authorization) to other participating institutions with the CKYC number. This helps avoid repetitive KYC processes every time you open a new account or invest in a different financial product.

CKYC is also commonly referred to as Central KYC in India and is part of the country’s broader digital financial infrastructure

The CKYC Ecosystem in India

CKYC India aims to create a single, unified view of an individual’s KYC status across all financial sectors—banks, mutual fund companies, insurance firms, and more. Specific regulations govern this ecosystem to ensure data privacy and security.

- Data security: CERSAI is responsible for maintaining secure records, ensuring that only authorized entities access your sensitive personal information.

- Regulatory oversight: The Reserve Bank of India (RBI), the Securities and Exchange Board of India (SEBI), and the Insurance Regulatory and Development Authority of India (IRDAI) have all mandated the use of CKYC for their respective financial sectors.

These regulatory bodies ensure that CKYC adoption remains standardized across the financial ecosystem.

Key Features of CKYC

- 14-digit CKYC number: Every individual completing CKYC is assigned a unique 14-digit number, often called a CKYC number or KIN (KYC Identification Number).

- Secure electronic storage: KYC data is stored digitally in a secure environment managed by CERSAI.

- Issuer verification: Documents submitted are verified with issuing authorities (e.g., Aadhaar, Passport, etc.) to ensure authenticity.

- Unified updates: All authorized financial institutions get notified automatically when you update your KYC information.

- Real-time file exchange: APIs provided to regulated entities facilitate instant KYC checks, accelerating account opening and transactions.

- Advanced user authentication: Access to the CKYC system requires secure credentials, minimizing data misuse.

CKYC also enables faster digital onboarding through integration with financial institutions’ internal systems.

The CKYC Registration Process

To become part of the CKYC system, you must undergo a CKYC registration. Here’s a simplified breakdown:

Initial KYC Submission

The first time you interact with a financial institution—be it a bank, NBFC, stock broker, or insurance provider—you’ll be asked to provide KYC details: PAN, proof of address, proof of identity, photograph, and other essential information.

Data Upload to CERSAI

Once your data is verified and your account is opened, the respective institution forwards your KYC information to CERSAI.

CKYC Number Allocation

Once CERSAI verifies the data, a 14-digit CKYC number is generated. CERSAI or the institution communicates the CKYC number to your registered mobile number and email address.

Centralized Storage and Access

Financial institutions can now refer to this centralized database using your CKYC number for any future KYC verification without asking you to repeat the entire process—unless there are changes to your details. You can generate your CKYC card on https://www.ckycindia.in/. Additionally, you can verify that your data was last updated by any financial institution.

Did You Know

When you move to another bank or financial service provider, you can simply share your CKYC number instead of re-submitting all the documents. The new institution can retrieve your verified KYC from the CKYC registry.

Important Notes:

- If there is an error or a mismatch in your data, your registration may get rejected. Always ensure your documents are up-to-date and correct to avoid delays.

- Financial institutions may require periodic re-verification or updates of KYC documents due to regulatory norms.

Did You Know

When you move to another bank or financial service provider, you can simply share your CKYC number instead of re-submitting all the documents. The new institution can retrieve your verified KYC from the CKYC registry.

Who Can Register Customers for CKYC?

Financial institutions regulated by:

- SEBI (Securities and Exchange Board of India)

- RBI (Reserve Bank of India)

- IRDAI (Insurance Regulatory and Development Authority of India)

- PFRDA (Pension Fund Regulatory and Development Authority)

Examples:

- Banks (public, private, small finance, payments banks)

- NBFCs (Non-Banking Financial Companies)

- Insurance companies

- Mutual fund houses

- Stockbrokers

If you open a bank account or invest in a mutual fund with any of these institutions, they’ll handle the CKYC registration process on your behalf.

How to Get Your CKYC Number

You don’t need to apply for a CKYC number separately. It is automatically generated when your KYC is submitted and verified by a financial institution registered under the Central KYC (CKYC) system. Here’s how you can ensure you receive it:

- Open a new account or investment with a bank, NBFC, mutual fund, or insurance company registered under CKYC norms.

- Submit accurate and complete KYC details (including PAN, address proof, etc.).

- Confirm if your institution has uploaded your details. You can usually request confirmation by contacting the organization’s customer support handling your KYC.

- Receive your CKYC number/KYC Identification Number (KIN). In some cases, you might get notified about your KIN via email or SMS. If not, you can request it from the financial institution you registered with.

How to Download Your CKYC Card

You can retrieve your CKYC card in two ways:

Via a Missed Call

Give a missed call to 7799022129 to receive your CKYC card via SMS (only works if your mobile number is linked).

Online Retrieval

- Visit the CKYC Portal and verify your registered mobile number.

- A download link for your CKYC card will be sent via SMS.

Why CKYC Matters

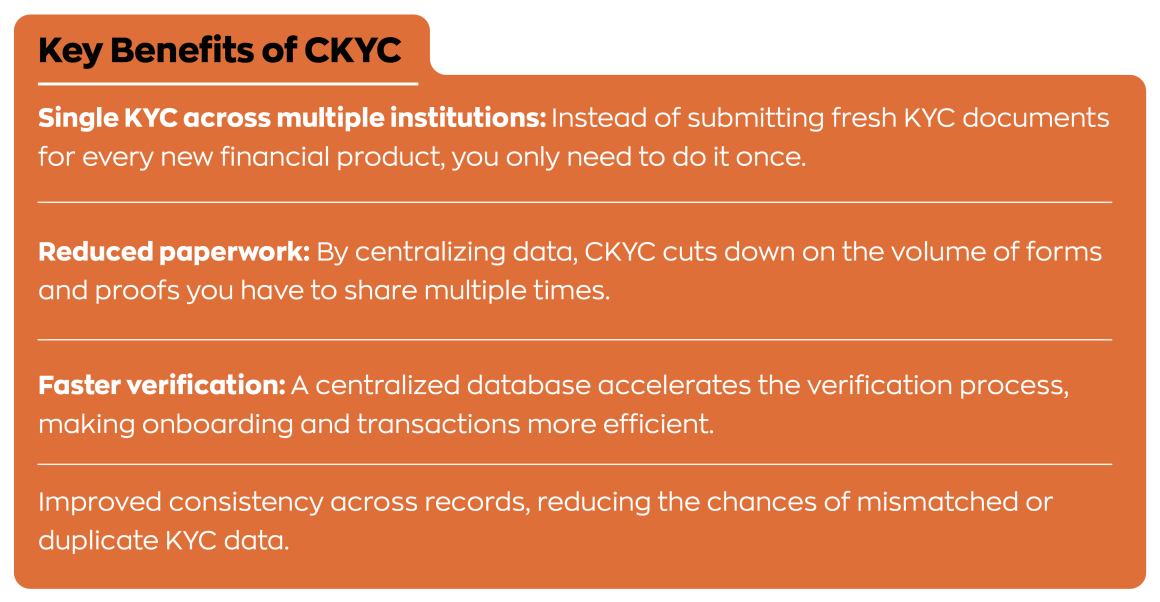

- Consistency: Having a single reference point avoids discrepancies between different accounts.

- Efficiency: A one-time verification drastically reduces the back-and-forth with documents.

- Security: Since only authorized entities under CERSAI can access your KYC data, it enhances the security of your personal information

For individuals who frequently open new financial accounts—whether for investments, loans, or insurance—CKYC is a game-changer. It’s a more streamlined and efficient process, saving both time and effort.

CKYC stands out as a robust solution to the repetitive KYC checks that financial consumers in India have long faced. By centralizing customer data in a secure repository, CKYC minimizes paperwork, speeds up account openings, and ensures consistency across various financial platforms.

For institutions striving to offer streamlined, secure, and user-friendly processes, incorporating CKYC into their workflows is a logical step. With platforms like Zwitch simplifying implementation, both businesses and customers can benefit from fast, reliable onboarding powered by CKYC.

Build faster onboarding journeys with Zwitch’s KYC APIs.

Frequently Asked Questions (FAQs)\

1. What is a CKYC?

CKYC (Central Know Your Customer) is a centralized system that stores KYC records of individuals in India, allowing financial institutions to access verified details from a single repository.

2. How do I get my CKYC number?

You don’t need to apply separately. Your CKYC number is generated automatically when you complete KYC with a registered financial institution such as a bank, NBFC, mutual fund, or insurance provider.

3. What is the difference between CKYC and eKYC?

CKYC is a centralized system where your KYC details are stored in a single repository (CERSAI) and can be reused across institutions. eKYC is a digital, Aadhaar-based method for instant, institution-specific verification. CKYC reduces repeated paperwork, while eKYC enables quick remote onboarding.

4. What are the key components involved in CKYC?

CKYC is based on core KYC processes that include verifying a customer’s identity, evaluating risk through due diligence, and maintaining updated records over time to ensure accuracy, compliance, and proper monitoring of customer information.

Interested in our APIs? Let’s talk!

Tell us your automation goals, and we’ll set you up with a free, personalized demo from our API expert.