Card payments power everyday transactions from groceries and fuel to online checkouts and subscriptions. But when something breaks in the payment chain, transactions can fail instantly, disrupting both businesses and customers.

These disruptions, often referred to as credit card processing outages, can create immediate challenges missed sales, delayed payments, and poor customer experiences. Even short downtime during peak hours can have a noticeable impact, especially for businesses that rely heavily on digital payments.

In this guide, we’ll break down:

- Why payment systems experience outages

- Where failures typically occur in the payment flow

- How these disruptions impact businesses and customers

- What you can do to stay prepared and minimize risk

Understanding how these outages play out and how to respond can help you maintain continuity when payment systems don’t behave as expected.

What Is a Credit Card Processing Outage?

A credit card processing outage refers to a situation where card payments either online or in-store temporarily stop working. It may affect all types of cards (debit, credit, prepaid) or just one network (like Visa or Mastercard). During an outage, point-of-sale (POS) machines might stop working, online payments may fail, and even ATM withdrawals can be affected in some cases.

These card outages usually occur due to issues at the payment processor, network failures, or disruptions in the banking infrastructure. When this happens, transactions may be delayed, declined, or not processed at all, often leading to frustration for both customers and merchants.

Depending on the cause, a credit card processor outage can last for a few minutes or extend to several hours.

Why Do Credit Card Outages Happen?

There isn’t a single cause. Card payment failures usually occur when something breaks across a multi-layered ecosystem. Here are the most common reasons:

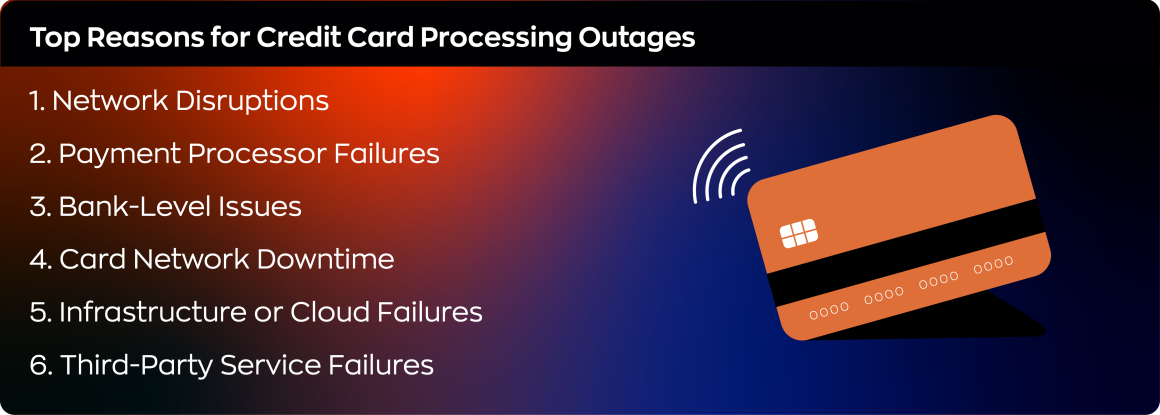

1. Network Disruptions

Every card transaction depends on stable internet connectivity across systems—from POS machines to payment gateways. Issues with telecom providers, DNS services, or data centers can disrupt this flow. Even short network failures can lead to a high volume of declined transactions.

2. Payment Processor Failures

Payment processors route transactions between card networks and banks. Software bugs, failed updates, or server overload during peak traffic can cause unexpected downtime. Even a small misconfiguration can impact transactions at scale.

3. Bank-Level Issues

Outages can also originate from the issuing bank. Scheduled maintenance, core banking system failures, or internal glitches can result in transactions being declined. This can happen even when merchant systems are functioning normally.

4. Card Network Downtime

Card networks like Visa or Mastercard act as the bridge between banks and processors. If there’s a disruption at this layer, it can affect transactions across multiple banks and merchants. These outages tend to have a wider, ecosystem-level impact.

5. Infrastructure or Cloud Failures

Modern payment systems rely heavily on cloud infrastructure and data centers. Power outages, hardware issues, or cloud service disruptions can bring parts of the system offline. This can temporarily halt transaction processing.

6. Third-Party Service Failures

Payment flows often depend on third-party services like fraud detection, authentication (OTP), and APIs. If any of these services fail or slow down, transactions may not go through. These dependencies can become hidden points of failure.

Impact on Businesses and Customers

The immediate impact is obvious: payments fail. But the effects go deeper than that.

For businesses, especially small retailers, an outage during busy hours means missed revenue. Many customers may not have alternative payment options and could walk away. Over time, frequent outages can also affect customer trust. If card payments keep failing, people may hesitate to shop from the same place again.

For customers, it leads to inconvenience and sometimes embarrassment. You might be in the middle of a purchase when your card gets declined for no fault of your own. For online transactions, it may mean missing a payment deadline or offer window.

What Can You Do During a Credit Card Outage?

Being prepared can make a big difference when these issues arise.

If You’re a Merchant:

- Keep Backup Options: Always have alternative payment modes ready — UPI, QR codes, net banking, or even cash. The more flexible you are, the less likely you’ll lose a sale.

- Stay Informed: Use a payment service provider that gives real-time updates about outages. Some platforms offer alerts or dashboards to monitor system health.

- Train Staff: Ensure your team knows how to handle failed transactions calmly and inform customers without creating panic.

- Record Transactions: In some cases, you may allow customers to pay later or record the transaction manually and complete it once systems are back.

If You’re a Customer:

- Carry Alternatives: Keep at least two payment options — a card and a UPI app, for instance. This reduces dependency on a single system.

- Know It’s Temporary: Most outages are resolved quickly. If a transaction fails, wait for a few minutes and try again.

- Check Before Blaming: If your card is declined, it may not be an issue with your account. Check with the merchant or look up recent news about any credit card processor outage.

- Report the Problem: If your bank’s app or card service continues to fail, report it to customer support for clarity.

Can These Outages Be Prevented?

Complete prevention isn’t realistic. The system involves multiple layers — banks, processors, card networks, telecom services, and internet connectivity. Outages can happen at any point in this chain.

However, their impact can be minimised. Businesses can choose reliable service providers known for uptime and quick response. They can also test their systems regularly and keep backup methods ready.

Banks and processors, on their part, continue to invest in better infrastructure, redundancy, and security. Regulators are also stepping in to ensure smoother, more resilient digital payments.

Don’t Let Payment Outages Catch You Off Guard

When a credit card processing outage hits, having a reliable backup isn’t optional it’s essential. Zwitch payment infrastructur that helps businesses stay operational no matter what. With support for 150+ payment methods including UPI, NEFT, IMPS, and RTGS, you’re never dependent on a single payment rail.

Zwitch’s Payment Gateway ensures faster checkouts and higher success rates, while its Payouts and Connected Banking features keep transactions moving across 150+ banks even when one network goes down. For businesses that can’t afford downtime, Zwitch gives you the flexibility and redundancy to keep payments flowing.

Explore Zwitch’s payment solutions.

Final Thoughts

Credit card outages may be rare, but when they strike, they disrupt both business and consumer experiences. The good news? With the right preparation, their impact can be managed — or even avoided.

As digital payments continue to grow, staying informed and flexible is key. For merchants, this means offering multiple payment modes and keeping track of system health. For customers, it’s about having a plan B — and understanding that sometimes, technology simply needs a moment to catch up.

FAQs

1. What typically causes credit card or payment processing outages?

Outages usually stem from failures across the payment chain—banking networks, payment gateways, processor downtime, or connectivity issues. In many cases, it’s not a single point of failure but a dependency breakdown across systems that aren’t fully integrated.

2. What should finance or ops teams check first during an outage?

Start by isolating the failure point. Check internal systems (POS, ERP, connectivity), then verify your payment provider or gateway status. If multiple systems are involved, lack of visibility can slow diagnosis—this is where unified monitoring becomes critical.

3. How can businesses continue accepting payments during an outage?

Continuity depends on having fallback options. This can include secondary payment gateways, offline transaction capture, or alternate rails like UPI or bank transfers. The key is not just having backups—but ensuring they are pre-configured and operationally ready.

4. How can businesses reduce the impact of payment outages?

Reducing impact is less about reacting fast and more about being prepared. Businesses should implement redundancy across payment providers, maintain real-time visibility into transaction flows, and automate failover where possible to avoid manual intervention during disruptions.

5. Why does relying on a single payment provider increase risk?

A single provider creates a single point of failure. If that provider experiences downtime, the entire payment flow is affected. Multi-provider setups add resilience, ensuring transactions can be routed dynamically, and revenue loss is minimized.