If you build payment flows, collections, or reconciliation systems, you already know that the hard part is rarely the payment itself. It’s the orchestration around it: confirming transaction context, triggering downstream updates, notifying finance teams, reconciling across ledgers, and generating audit-ready records without someone manually stitching data together across tools.

That orchestration has traditionally relied on custom glue code for dozens of point-to-point integrations, each one fragile and maintained separately. Every new AI tool your team wants to connect adds another connector to build and another surface to manage.

In 2026, there is a cleaner way to approach this. It’s called the Model Context Protocol, and it is changing how MCP for payment developers is enabling AI-assisted financial workflows across industries.

This article explains what MCP is, how it works, why MCP for payment developers matters when integrating with Indian payment infrastructure, and how it opens the door to truly connected banking experiences for modern enterprises.

The Integration Problem That MCP Was Built to Solve

Before MCP, connecting an AI model to external systems, a payment gateway, a CRM, a document store, and a ledger required building a custom connector for each pairing. If you had five systems and wanted an AI agent to work across them, you needed connectors for every combination.

Anthropic described this as the N×M data integration problem: N models, M tools, each requiring its own bespoke implementation. The complexity compounds every time you add a new AI client or a new data source.

The Model Context Protocol, introduced by Anthropic in November 2024 and open-sourced immediately, collapses that complexity from N×M down to N+M. You expose your payment system as a single MCP-compliant server once, and any MCP-compatible AI client can discover and invoke its capabilities without you writing another connector.

Think of it as the USB-C of AI integration: a universal adapter that removes the combinatorial integration tax from your development roadmap.

Within twelve months, the protocol had been adopted by every major AI platform. By March 2026, the MCP SDK was logging over 97 million monthly downloads across Python and TypeScript, with more than 10,000 active public MCP servers listed in the official registry. OpenAI, Google DeepMind, Microsoft, and AWS all added native MCP support.

In December 2025, Anthropic donated MCP to the Agentic AI Foundation under the Linux Foundation, a clear signal that this is infrastructure, not a vendor feature.

How MCP Actually Works: The Architecture in Plain Terms

At a high level, MCP defines three roles in every integration: the host, the client, and the server.

- The MCP host is the AI-powered application, an agent, chatbot, or workflow engine, that needs to take action.

- The MCP client is the layer within that host that manages connections and handles protocol mechanics.

- The MCP server is the system exposing capabilities, your payment gateway, property management system, or accounting platform.

When an AI agent needs to initiate a payment verification, check an installment schedule, or pull a reconciliation report, it sends a standardized JSON-RPC 2.0 request to the relevant MCP server. The server responds with structured data, and the agent uses that response to decide the next step.

What matters here is not just the request-response cycle, but the fact that this entire interaction happens within a framework that requires user consent before any tool executes.

For payment developers, the implication is simple but powerful: you build your payment capabilities as an MCP server once, and any MCP-compatible AI system, internal or external, can use them without additional integration work.

Why the Payment Industry Is Moving Toward MCP

The payment rails problem is largely solved. In India, digital payments accounted for 99.8% of total transaction volume in H1 2025, with UPI alone handling 85% of that volume, growing 35% year-on-year. Globally, wallet payments made up 54% of e-commerce transaction volume in 2023 and are projected to hit 61% by 2026. The infrastructure works. What has not kept pace is the intelligence layer that sits on top of it.

Payment systems are still largely reactive. A transaction comes in, a webhook fires, your backend processes it, and downstream systems are updated in a fixed sequence. There is no contextual reasoning, no dynamic decision-making, no ability for the system to understand what the payment means in the broader context of a customer relationship or business workflow.

Consider what a complex payment workflow typically involves:

- Multi-step collections tied to milestones or approvals

- Payout coordination across vendors, accounts, or settlement cycles

- Reconciliation across multiple systems and ledgers

- Compliance checks tied to transaction limits, KYC, or regulatory thresholds

These are not linear flows. They are multi-step, multi-system processes that require constant coordination.

MCP acts as the connective layer across these systems. When payment capabilities, such as initiating a transaction, verifying status, triggering refunds, or generating reconciliation reports, are exposed as MCP servers, an AI agent can orchestrate the entire lifecycle without custom integration logic between each system.

The shift this enables is subtle but important: from reactive systems that respond to events, to autonomous workflows that can reason and act across the full transaction context.

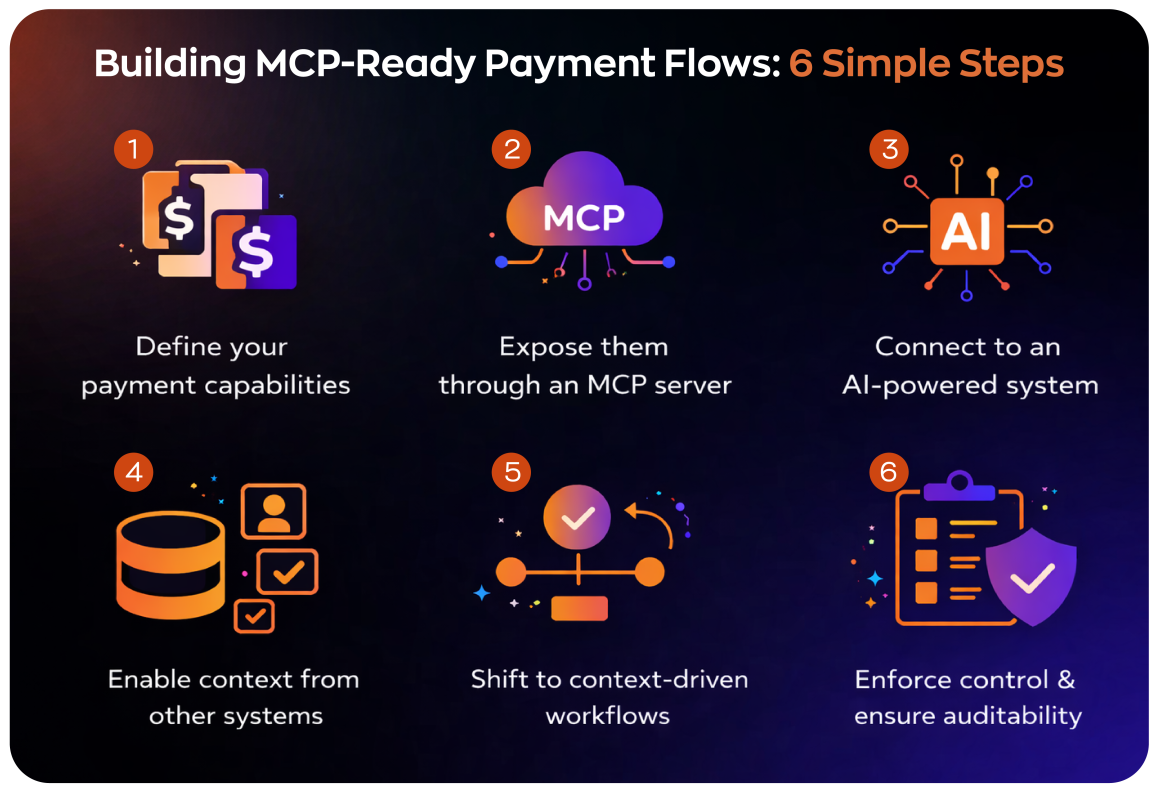

Building MCP-Ready Payment Flows: What It Looks Like in Practice

At a practical level, building MCP-ready payment infrastructure is less about rewriting your stack and more about how you expose and orchestrate capabilities across systems. It typically unfolds in a few clear steps.

1. Define your payment capabilities

Start by breaking your payment system into clear, reusable actions. Instead of thinking in terms of endpoints, think in terms of what an external system or agent should be able to do. This typically includes actions like initiating payments, verifying status, triggering refunds, generating reports, or fetching transaction data. These capabilities form the foundation of your MCP layer.

2. Expose them through an MCP server

Once defined, these capabilities are exposed as structured tools via an MCP server. Each tool has a clear schema and connects back to your existing payment APIs. You are not replacing your integrations here; you are standardizing how they are accessed and consumed.

3. Connect to an AI-powered system

With the MCP server in place, it becomes discoverable by any MCP-compatible AI system, whether that is an internal workflow engine, a support assistant, or an automation agent. Your payment infrastructure is now accessible beyond traditional API calls.

4. Enable context from other systems

Payments rarely operate in isolation. To make workflows meaningful, agents need context from systems like CRM, accounting, fraud detection, or internal databases. Each system can expose its own MCP server, allowing the agent to access and combine context dynamically across sources.

5. Shift to context-driven workflows

Instead of hardcoding flows, the agent uses available context to decide what actions to take and when. A single workflow might involve verifying a transaction, checking related data, triggering follow-up actions, and updating multiple systems, without a fixed sequence defined in code. This is where MCP shifts systems from event-driven execution to context-driven orchestration.

6. Enforce control and ensure auditability

Even in autonomous workflows, control remains critical. MCP allows you to define approval layers, permission boundaries, and execution constraints for sensitive actions. At the same time, every interaction is structured and traceable, making auditability a built-in outcome rather than a separate effort.

How Zwitch Is Built for the Agentic Payment Stack

Most payment gateways were designed for a world where developers call APIs manually, and workflows are hardcoded. Zwitch is built differently — as an API-first infrastructure layer where every capability is designed to be invoked programmatically, making it a natural fit for MCP-compatible orchestration.

For an AI agent to manage payments autonomously, it needs more than a checkout button. It needs access to the full payment lifecycle — collections, payouts, reconciliation, verification, and settlement — through clean, composable APIs. Zwitch exposes exactly that:

- Collections via Payment Gateway, UPI Intent APIs, Dynamic QR, Auto Collect (virtual accounts), and Payment Pages

- Payouts via Payout API and Connected Banking — link existing bank accounts and initiate transfers in real time

- Reconciliation built in — Auto Collect handles matching automatically, without manual intervention

- Verification micro-services — PAN, Bank Account, VPA, and Name Match APIs to validate context before transactions execute

- Settlement controls — Instant Settlements and Marketplace Split Settlements for platforms managing multi-party flows

Each of these is an API call. Which means each of these can be a tool in an MCP server — accessible to an AI agent as part of a larger, context-driven workflow. That is the architecture MCP makes possible, and Zwitch provides the payment primitives to build it on.

Security and Governance: What Payment Developers Need to Know

MCP’s rapid adoption has brought real security considerations to the forefront, especially for payment use cases, where the cost of incorrect actions is high.

The most significant risk is prompt injection. A compromised or malicious MCP server can return manipulated content designed to influence an AI agent’s behavior. In a payment context, this is not theoretical. An agent with access to initiate transactions, if fed incorrect context, could be led to take actions the user never intended.

At the same time, MCP is designed with important safeguards that are particularly relevant for financial workflows.

First, credentials remain isolated. API keys and payment credentials are stored within the MCP server and are never exposed to the model. The AI only interacts with structured outputs from tool calls, not the underlying sensitive data.

Second, MCP supports human-in-the-loop approval mechanisms. High-value or irreversible actions can be gated behind explicit user authorization. In payment workflows, this is not optional, and MCP provides a structured way to enforce it.

That said, the protocol defines the framework, but not the implementation guarantees. While MCP requires user consent before tool execution, how strictly this is enforced depends on the system’s design.

The March 2026 MCP roadmap reflects this reality. Enterprise-grade authentication, auditability, and gateway patterns are active areas of development, particularly because these gaps matter most in regulated environments like financial services.

For payment developers, the practical approach is familiar but critical:

- Treat MCP access scopes the same way you would treat OAuth permissions

- Grant only the minimum required access for each workflow

- Log every tool invocation for traceability

- Validate server identity before establishing connections

- Stay aligned with evolving security specifications and working group guidance

The MCP roadmap is publicly available and worth reviewing for any team making infrastructure decisions around agentic payment workflows.

The Practical Starting Point for Your Team

You do not need to rebuild your entire payment stack to participate in the MCP ecosystem. The realistic starting point for most payment development teams is to identify one workflow that currently requires manual coordination across multiple systems, and expose the relevant payment capabilities as a simple MCP server.

A simple MCP-enabled reconciliation assistant can:

- Query payment status

- Match transactions against business records

- Flag discrepancies in real time

This kind of implementation is bounded, auditable, and immediately valuable. More importantly, it gives your team hands-on experience with MCP without introducing unnecessary complexity.

From there, the model scales naturally. Each additional system you expose as an MCP server increases the overall capability of your architecture, without increasing integration overhead.

What This Means If You Are a CFO, Not a Developer

Most of what you have read so far is written for engineers. But if you are a CFO or finance leader, MCP has direct implications for your financial operations, and they are worth understanding before your technology team makes infrastructure decisions on your behalf.

Payment visibility across the full transaction lifecycle

One of the most persistent problems in finance operations is that payment data lives across too many systems. Gateway dashboards, accounting platforms, bank portals, and CRM records each have a partial view. Reconciling them at month-end is manual, slow, and error-prone. Discrepancies surface late, and by then, they have already created downstream problems.

MCP-enabled workflows change this by allowing a single AI agent to pull authoritative data from each of these systems in real time. The reconciliation that currently takes your finance team two days at month-close becomes a daily automated report, with discrepancies flagged as they occur, not after the books have closed.

Control without slowing down operations

A common concern among CFOs when AI enters financial workflows is the loss of control: if an agent initiates payments or triggers refunds autonomously, who is accountable? MCP addresses this directly through human-in-the-loop approval gates; high-value or irreversible transactions require explicit authorization from a named approver before execution. You define the thresholds. The system enforces them. Your audit trail is clean by design, not reconstructed after the fact.

Reduced integration cost as a finance line item

Every bespoke payment integration your engineering team builds is a maintenance liability on your balance sheet. It breaks when the upstream API changes. It requires developer time to fix. It creates delays in launching new financial products, automated reconciliation, payout workflows, and compliance reporting, because the underlying plumbing has to be rebuilt each time.

MCP reduces that liability by making your payment infrastructure composable. The finance team can request new automated workflows without commissioning new integration projects. For a CFO managing technology spend, that is a structural reduction in both capex and the opportunity cost of delayed financial product launches.

Compliance and auditability as a protocol feature

In regulated environments, the ability to produce a complete, timestamped audit trail of every payment action, who initiated it, what data was available at the time, and what approval was given, is non-negotiable. MCP’s architecture, with structured tool invocations and server-side logging, makes this audit trail a natural output of the system rather than something your team reconstructs manually for every regulatory query.

Frequently Asked Questions

1. Is MCP specific to a particular AI model or provider?

No. MCP is an open standard, now governed by the Agentic AI Foundation under the Linux Foundation, with co-founders including Anthropic, Block, and OpenAI. All major AI platforms, including Claude, ChatGPT, Gemini, and Microsoft Copilot, support MCP. Your MCP server works across all of them.

2. How does MCP differ from a standard REST API?

A REST API is a fixed interface that a developer calls programmatically. An MCP server is a discoverable interface that an AI agent can invoke dynamically, based on the context of what it is trying to accomplish. MCP also includes a standardized capability discovery mechanism, so an agent can understand what a server can do without you documenting every endpoint manually.

3. Do we need to replace our existing payment gateway integration to use MCP?

No. You build an MCP server as a layer on top of your existing integration. Your current gateway integration continues to work as it does. The MCP server simply exposes selected capabilities from that integration to AI agents in a standardized way. The two layers are independent.

4. Is MCP production-ready for financial services use cases?

MCP is in active production use across financial services globally, with Worldpay, Stripe, and Block among the known implementations. That said, the protocol’s enterprise security features, specifically around authentication, audit trails, and gateway patterns, are actively being formalized through the 2026 Working Group process. Teams building payment implementations should incorporate their own audit and access control layers in the near term, rather than waiting for the spec to fully address enterprise requirements.

5. What is the implementation effort for building an MCP server for a payment platform?

For a developer familiar with REST API development, building a basic MCP server using the official Python or TypeScript SDK is a matter of days, not weeks, for a focused set of capabilities. The MCP SDK handles all protocol mechanics; your work is defining the tool schemas and writing the handlers that call your underlying payment APIs. This is meaningfully faster than building a custom AI plugin from scratch for each AI platform. More complex implementations involving multi-system orchestration and enterprise-grade authentication will take longer, but the baseline is accessible for any backend development team.

MCP for payment developers is not a future consideration; it is a current infrastructure decision. The protocol is mature, the ecosystem is large, and the teams adopting it now are building payment workflows that their competitors will be scrambling to replicate in twelve months. The integration tax is not going away on its own. MCP is how you stop paying it.