The Payment Method Customers Actually Complete

Here’s a familiar scenario: your checkout flow is fast. Your design is clean. Everything works. And yet, conversions drop at the final step.

Not because customers changed their minds, but because the payment experience felt clunky, unfamiliar, or slow.

In India’s digital economy, where UPI powers over 80% of all retail digital payments, the last mile of checkout is where decisions are made—or lost. Small moments of friction here can directly impact conversion, revenue, and customer trust.

This is exactly where the choice between UPI intent vs dynamic QR becomes critical.

Two payment methods dominate this moment: UPI Intent and Dynamic QR. Both are reliable. Both are secure. But they work very differently, and choosing the right one—or more realistically, the right combination has a measurable impact on how customers complete payments.

This guide cuts through the technical noise. We’ll show CFOs, finance controllers, and product leaders how Intent and QR differ, where each performs best, and how to design a checkout strategy that balances speed, security, and scale. You’ll also find a practical framework to help you decide what fits your platform.

What is UPI Intent Payment?

UPI Intent is simple: your app or website redirects the customer directly to their UPI app (PhonePe, Google Pay, Paytm, WhatsApp Pay, etc.) with the transaction details already filled in. One tap. One PIN. Done.

Instead of typing a UPI address or scanning something, the customer lands inside their banking app, which they already trust and use daily. The amount, merchant name, and transaction ID are pre-populated. There’s nothing for them to enter. This is why it converts better.

How it works:

- Customer hits “Pay with UPI” on the checkout

- Your backend generates a UPI deep link (looks like: upi://pay?pa=merchant@upi&pn=Merchant&am=500…)

- Customer is instantly redirected to their UPI app

- They see the amount, verify it, and enter their PIN

- Payment confirms. They’re redirected back to your platform.

The psychology here matters: customers are using *their* app, not some new interface. That familiarity reduces friction dramatically.

What is Dynamic QR Payment?

A Dynamic QR code is a unique, single-use QR code generated per transaction. Unlike static QR codes (which stay the same forever), each dynamic QR is different, with the amount, merchant details, and a transaction reference baked in. It expires quickly and can’t be reused.

The customer scans it with their UPI app. The amount is pre-filled and locked (they can’t edit it). They see the merchant details and hit confirm. Simple, but it requires one extra action: the scan.

How it works:

- Customer reaches checkout on your website or app

- Your backend generates a unique QR code with the transaction amount embedded

- The customer opens their UPI app and scans the QR

- Amount is pre-filled and non-editable. Merchant is visible.

- Customer enters PIN. Transaction completes.

On the surface, both methods achieve the same outcome. But the experience, and the results, are noticeably different.

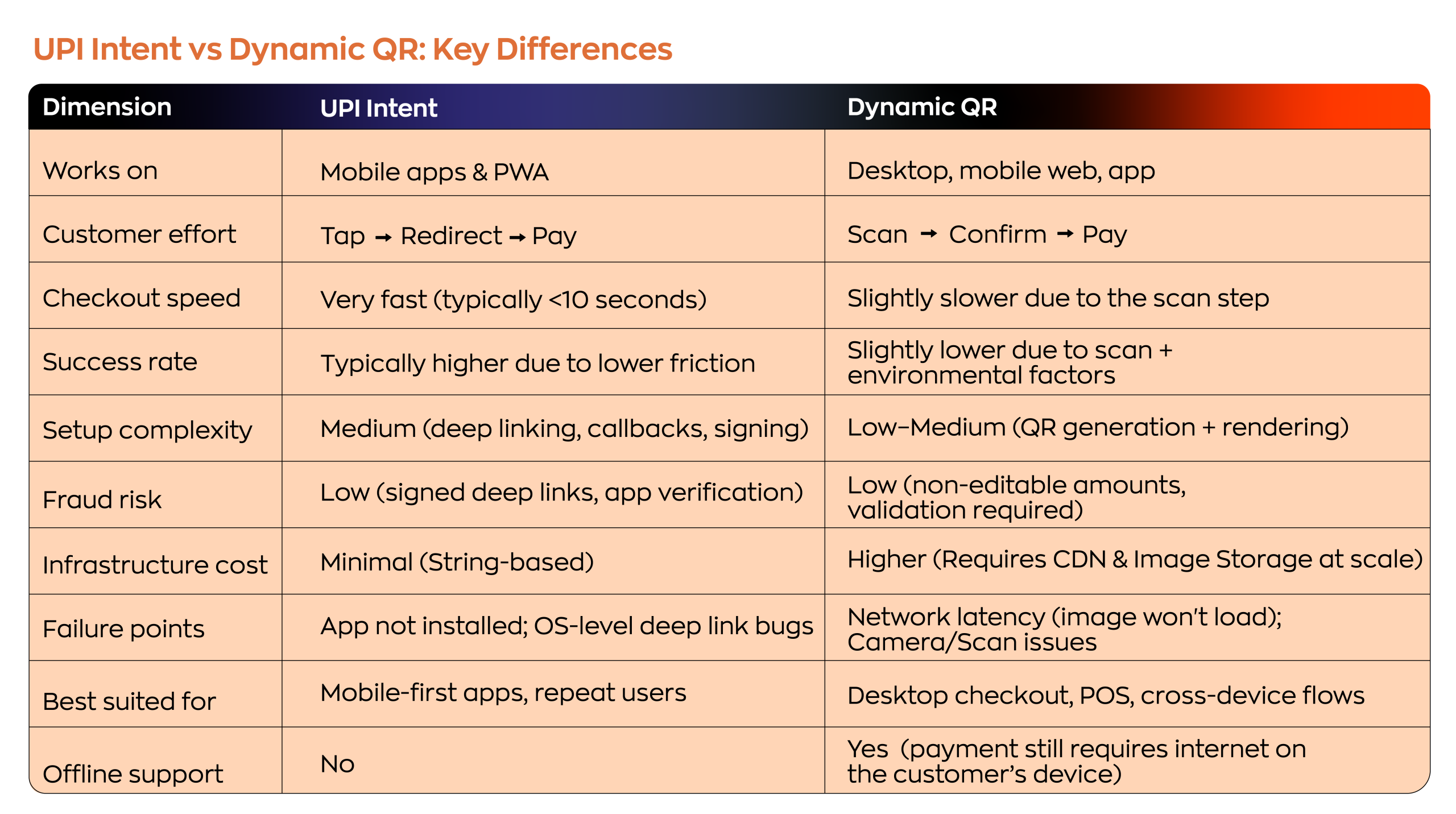

UPI Intent vs Dynamic QR: Key Differences

Which Drives Better Conversion?

Here’s what matters to your finance team: Even a small improvement in checkout completion rate compounds directly into revenue. For a platform processing ₹10 crore a month, a 2% lift means ₹20 lakh in recovered revenue — without acquiring a single new customer.

Why UPI Intent Wins on Conversion

- Zero friction: Customers tap once and land inside their trusted UPI app. They recognize the interface immediately.

- Higher success rates: Eliminates typing errors, SMS notification delays, and payment failures.

- Speed matters: Total checkout time is <10 seconds for returning customers.

- Psychology: When customers see their app open, they feel safe. That trust signal converts.

Where Dynamic QR Excels

- Universal coverage: Works on desktop, mobile web, old browsers, feature phones, everywhere.

- No app dependency: If a customer doesn’t have UPI installed, Intent fails. QR always works as a fallback.

- Offline ready: Print it, display it, embed it. No connectivity is needed to show a QR code.

- Data visibility: Every scan is logged. You get granular insights into your checkout funnel.

The smart play: Use both. Mobile app users see Intent. Desktop users see QR. This “smart routing” is now standard for mature platforms.

Implementation: What Your Engineering Team Should Know

Implementation complexity directly affects launch timeline and long-term maintenance. Here’s the real story:

UPI Intent Setup

- Generate signed deep links server-side with transaction data

- Handle app-specific deep links (bhim://, paytm://) or generic upi:// URIs

- Implement callback/polling to confirm payment status when the user returns

- Store signing keys securely (HSM recommended) to prevent tampering

Dynamic QR Setup

- Call the QR generation API with the transaction amount and merchant details

- Display QR image on checkout page

- Poll for transaction status once QR appears

- Set expiry timers (typically 5–10 minutes) to prevent stale scans

Bottom line: Intent requires stronger cryptographic chops. QR is faster to launch but requires stateless QR generation and image management. For teams adding payment infrastructure for the first time, QR is simpler. For teams with security expertise, Intent is cleaner long-term.

Scaling: What Breaks at 100k Transactions/Day?

Payment methods that work fine at 1,000 txns/day can buckle at 100,000 txns/day. Here’s what scales and what doesn’t:

UPI Intent at Scale

- Network Load: Minimal. One lightweight deep link string per transaction. No image assets to load.

- Storage: Zero. Only transaction metadata is stored in the DB.

- User Experience: High consistency. No risk of “broken images” or slow loading on poor connections.

Dynamic QR at Scale

- Infrastructure Cost: Higher. Generating, hosting, and serving 1 million QR images daily requires significant CDN and Object Storage (S3/GCS) costs to ensure the QR renders in under 2 seconds.

- Network Latency: In low-network areas, loading a 20KB QR image can fail or lag, leading to “abandonment at the finish line.”

- Database Impact: High. Constant polling for QR status creates a significant read-load on transaction tables.

Smart scaling strategy: Use Intent for app users (minimal load). Use cached QR for web users (reuse identical QR for similar amounts within 60-second windows). Monitor both and optimize separately.

Security: Where Each Method Fails

Both are secure when implemented correctly per NPCI guidelines. But they fail in different ways:

UPI Intent Vulnerabilities

- Phishing: A compromised website can generate fake Intent links. Mitigation: Validate all intent parameters server-side and rely on app-level verification supported by UPI apps.

- Deep-link hijacking: Malicious apps can intercept upi:// schemes. Mitigation: Use App Links (Android) or Universal Links (iOS) tied to domain ownership.

- Silent failures: No UPI app installed means a silent failure with no fallback. Mitigation: Always provide a QR fallback.

- Regulatory: NPCI tightened UPI rules significantly in 2025 — banning P2P collect requests from October 2025 and introducing stricter API governance for all payment providers. The direction is clearly toward Intent-first flows on mobile. If your platform still relies on manual VPA entry or collect-based flows, review your integration against the current NPCI guidelines.

Dynamic QR Vulnerabilities

- Physical swap: Attacker replaces your QR with theirs. Mitigation: Display merchant name + amount clearly in UI. Educate users to verify.

- Slow rendering: Slow QR generation >3 seconds, which frustrates users. Mitigation: Cache aggressively, lazy-load images.

- Expiry & reuse: QR codes must expire (5–10 min). A stale QR can be reused. Mitigation: Regenerate on refresh, validate state in backend.

- Amount lock (feature, not flaw): QR amounts are non-editable. If the display amount is wrong due to a bug, QR locks it in. Mitigation: Validate amounts before QR generation.

What the Numbers Tell Us

Here’s what the market is actually doing (2025 data):

- UPI processed 228 billion transactions (₹300+ lakh crore) in 2025, the world’s largest real-time payment system by volume.

- QR-based payments: While QR adoption is widespread, Intent-based flows consistently outperform QR in mobile environments by mitigating environmental failures such as camera issues, poor lighting, and scan errors.

Translation: The market has matured. QR isn’t a niche feature anymore; it’s foundational. But Intent is the growth lever. Platforms without Intent on mobile are leaving measurable revenue on the table.

For full regulatory details, see NPCI’s Official UPI Linking Specifications: https://www.npci.org.in/

How Zwitch Simplifies Your Payment Strategy

Managing UPI Intent and Dynamic QR at scale is not just about enabling payments; it’s about orchestrating multiple collection methods, ensuring reliability, and keeping reconciliation effortless for finance teams. Zwitch brings all of this together into a single, unified payments infrastructure designed for enterprise-grade scale and simplicity.

Here’s what Zwitch enables:

- Seamless UPI acceptance: Support for Intent APIs, merchant collect requests, and dynamic QR strings to ensure smooth UPI checkout across mobile and web.

- Flexible payment collection: Create payment links and custom checkout pages instantly without heavy engineering effort.

- Automated collections & reconciliation: Virtual accounts (Auto Collect) help map, track, and reconcile incoming payments automatically.

- Built-in scalability: From instant settlements to marketplace fund splits, Zwitch supports complex money movement flows without additional infrastructure overhead.

The result: A single system that handles how money is collected, routed, and settled, without stitching multiple tools together.

Explore how Zwitch simplifies UPI checkout integration and improves payment UX optimization for your platform.

Get started now!

How to Choose: A Decision Framework

Here’s the straightforward framework for your team. Use this to decide which method, or combination, fits your platform:

- Mobile-first platform (app, PWA, in-app checkout)?

Prioritize UPI Intent. It reduces cart abandonment and delivers the fastest checkout. Offer QR as a fallback for users without the UPI app installed.

- Cross-device platform (desktop + mobile)?

Implement smart routing: Intent for mobile app/PWA users, QR for desktop and mobile web. Use a unified API to avoid maintaining two separate integrations.

- Offline or low-bandwidth use case?

Use Dynamic QR. Customers can print it, display it, and scan it offline. Perfect for point-of-sale, hyperlocal commerce, and rural payments.

- High-volume, cost-sensitive platform?

Intent. Lower per-transaction cost, faster processing, minimal infrastructure overhead. Especially important for recurring billing, B2B, and loan repayments.

- Multiple use cases or unsure?

Use both. Smart routing is no longer optional; it’s standard. Most mature platforms support Intent + QR with intelligent device detection.

The Bottom Line

UPI Intent and Dynamic QR aren’t competitors. They’re complementary tools optimized for different contexts. Choosing one over the other is the wrong question. The right question is: How do I serve the optimal method to each customer?

If you’re mobile-first: Intent is non-negotiable. If you operate cross-device, implement both. If you’re cost-sensitive, Intent scales cheaper. If you operate offline, QR is your answer.

The platforms winning right now aren’t choosing between Intent and QR. They’re orchestrating both intelligently, monitoring both separately, and optimizing both continuously. That’s where the conversion gains come from.

Your customers don’t care which method you use. They care that checkout is fast, secure, and doesn’t make them think. Focus there, and you’ll win.

FAQs

What’s the core difference between Intent and QR?

Intent redirects the customer directly into their UPI app with pre-filled details (tap to pay). QR requires the customer to scan a code within their UPI app (scan to pay). Intent is faster but mobile-only. QR works everywhere.

Which is more secure?

Both, when implemented per NPCI guidelines. Intent uses cryptographic signing to prevent tampering. QR has non-editable amounts. They fail in different ways (Intent: deep-link hijacking; QR: physical code swap). Neither has an inherent security advantage; it’s about implementation quality.

Can I use both at the same time?

Yes, and you should. Serve Intent to mobile app users, QR to web users. This “smart routing” is now industry standard. It maximizes conversion across all customer segments.

What does the NPCI mandate mean for my platform?

NPCI has been actively tightening UPI rules through 2025. P2P collect requests were banned from October 1, 2025. Separately, OC 215/2025-26 mandated strict API governance for all PSPs from August 2025. Industry guidance strongly recommends Intent as the standard for mobile-native checkouts. Review your current integration against NPCI’s latest circulars to ensure compliance.

How much better is Intent for conversion?

Intent consistently outperforms QR codes in mobile environments, primarily by removing friction points such as scanning, camera errors, and manual entry. The exact lift varies by platform, but the direction is clear — fewer steps means fewer drop-offs.