Agentic commerce is redefining how payments work by allowing AI agents in payments to initiate, decide, and execute transactions autonomously. For Indian businesses, this means fewer manual interventions, smarter cash flow management, and payments that are triggered at the right time — with reduced manual intervention under defined controls. This blog explains what agentic commerce is, how autonomous payments work in India, and how businesses can prepare for the future of payments.

What Is Agentic Commerce?

Agentic commerce refers to an emerging model of AI-driven commerce where software agents can evaluate context, apply predefined policies, and initiate actions — including financial transactions — on behalf of users or businesses.

In payments, this means:

- AI agents monitor operational data (inventory, invoices, subscriptions, usage patterns)

- Evaluate conditions such as due dates, limits, and liquidity

- Trigger transactions programmatically through secure, compliant APIs

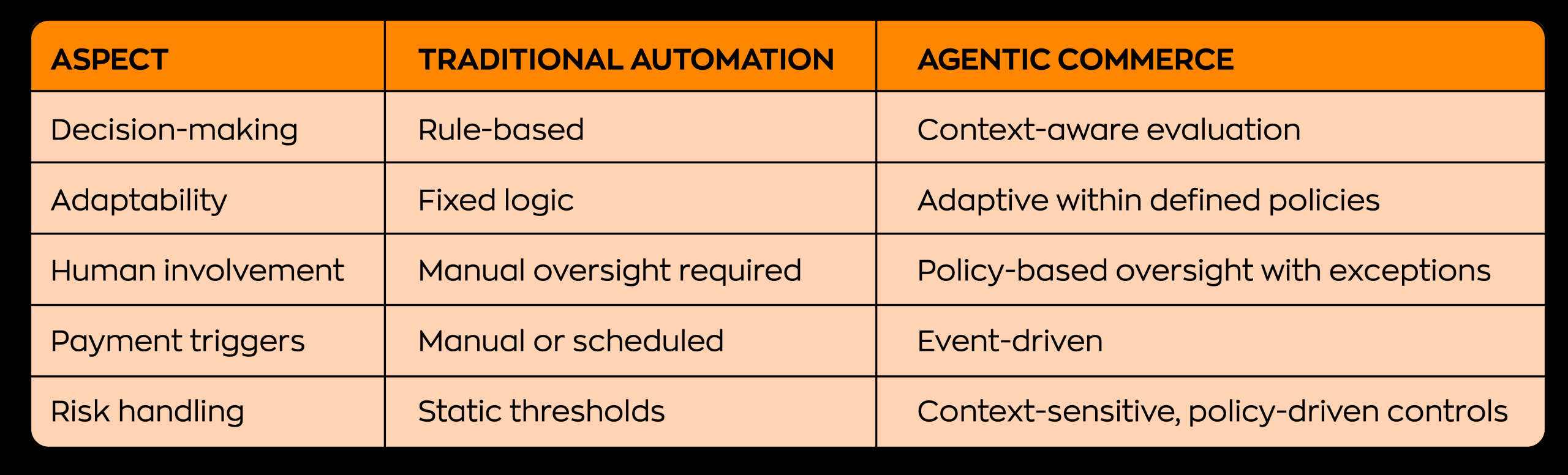

Unlike traditional rule-based automation, AI agents in payments can incorporate contextual analysis and adaptive logic within defined risk and regulatory boundaries.

Why Agentic Commerce Is Gaining Momentum in India

India’s digital payments ecosystem is strongly positioned for agentic commerce due to three major factors:

1. API-first financial infrastructure

India has built a foundation of interoperable financial systems, including:

- UPI for real-time payments

- The Account Aggregator framework for consent-based financial data sharing

- Banking and payment APIs enabling programmatic, near real-time execution

These rails make it technically feasible to design event-driven, policy-based payment workflows.

2. SMBs are digitising faster than ever

Across sectors, Indian SMBs are increasingly adopting:

- Accounting and ERP software

- Subscription-based SaaS tools

- Digital lending platforms

- Online procurement and vendor management systems

As operational data becomes digitised, it creates a favourable environment for policy-driven autonomous payments triggered by software signals.

3. Growing operational complexity

Manual approvals become difficult to scale when:

- Vendors are paid frequently

- Inventory cycles are short

- Subscriptions renew automatically

- Compliance deadlines are strict

Within defined controls, agentic systems can reduce operational load and improve payment efficiency.

From Automation to Autonomy: What’s the Difference?

While automation follows fixed instructions, agentic commerce assesses context and initiates actions within clearly defined operational and regulatory frameworks.

How Agentic Commerce Operates Within Modern Payment Infrastructure

Step 1: Data intake

AI agents consume inputs such as:

- Invoices

- Inventory levels

- Subscription usage

- Credit limits

- Cash flow data

Step 2: Policy and context evaluation

The system evaluates predefined conditions, including:

- Whether a payment is due

- Invoice validation checks

- Liquidity thresholds

- Approval requirements

- Compliance constraints

Step 3: Compliant payment initiation

Once conditions are satisfied, the system initiates payment requests through approved rails such as:

- UPI e-mandate flows

- Bank transfer APIs

- Card payment gateways

- Virtual account settlements

All actions remain subject to authentication, mandate, and regulatory requirements.

Step 4: Feedback & optimisation

The system can incorporate feedback signals, such as payment failures, delays, or liquidity constraints, to refine policies and improve future decision-making within defined risk controls.

Why Agentic Commerce Matters for Indian Businesses

Faster cash flow cycles

Payments can be initiated as soon as predefined conditions are satisfied, rather than waiting for manual intervention.

Lower operational costs

By reducing manual reconciliation, follow-ups, and exception handling, finance teams can operate more efficiently and with fewer errors.

Improved compliance

Policy-driven payment workflows can be configured to align with:

- GST timelines

- Vendor contract terms

- Internal approval hierarchies

- Applicable regulatory requirements

Better Financial Intelligence

Structured, event-driven payment data creates a continuous feedback loop, enabling improved forecasting, working capital visibility, and policy refinement.

Risks & Considerations to Be Aware Of

Agentic commerce is not plug-and-play. Successful implementation requires clearly defined policies, governance controls, and regulatory alignment.

1. Inadequate guardrails

Poorly configured automation can result in:

- Duplicate payments

- Liquidity strain

- Policy or compliance breaches

Strong approval hierarchies, transaction thresholds, and exception handling workflows are essential.

2. Data privacy & consent

Policy-driven payment systems rely on access to financial and transactional data. Businesses must ensure:

- Explicit user consent where required

- Secure API integrations

- Alignment with applicable RBI and data protection regulations

3. Explainability & auditability

Organizations should be able to clearly understand:

- Why a payment was initiated

- Which policy conditions were satisfied

- What approvals or mandates were applied

Opaque or poorly documented decision logic increases operational and compliance risk.

Best Practices for Implementing Agentic Commerce

1. Start with controlled, low-risk workflows

Begin with narrowly scoped use cases such as:

- Low-value recurring payments

- Subscription renewals

- Vendor retainers

These controlled environments allow businesses to validate policies, monitor system behaviour, and refine approval logic before expanding to higher-value or more complex payment flows.

2. Define clear decision boundaries

Establish explicit policy constraints, including:

- Maximum transaction limits

- Time-based approval requirements

- Predefined exception handling rules

- Escalation pathways for policy breaches

Clear boundaries ensure the system operates predictably and within defined governance frameworks.

3. Maintain human oversight during early stages

In initial phases, use automated systems for policy-based initiation while retaining human review for exceptions and higher-risk transactions.

Gradually reduce manual intervention only after sufficient monitoring, auditability, and performance validation.

4. Invest in API-first infrastructure

Agentic commerce relies on infrastructure that supports:

- Real-time payment APIs

- Webhooks and event notifications

- Reliable mandate and authentication workflows

- Event-driven triggers

Without modern API connectivity, contextual payment initiation is difficult to implement reliably.

Explore Zwitch’s payment APIs.

Agentic Commerce and the Future of Payments

The future of payments is likely to become more contextual, event-driven, and policy-aware.

Instead of being manually initiated at fixed intervals, payments may increasingly be triggered automatically when predefined conditions are met.

Decision-making can become more continuous and data-informed, rather than dependent on periodic reviews or manual intervention.

As operational execution becomes more automated, finance teams can shift their focus from routine processing to liquidity strategy, risk management, and financial planning.

Agentic commerce represents a transition from manually executing payments to intelligently orchestrating them within defined governance frameworks.

How Zwitch Fits into the Agentic Commerce Stack

Zwitch provides API-first payment infrastructure that enables businesses to integrate UPI, virtual accounts, and payout capabilities directly into their systems. With developer-ready APIs and real-time transaction visibility, businesses can design payment workflows aligned with their own policies and operational controls. This API-driven connectivity supports modern, system-integrated payment architectures required for contextual and policy-based payment orchestration.

👉 Explore Zwitch’s payment APIs to build agent-ready payment flows.

Frequently Asked Questions (FAQs)

1. What is agentic commerce in payments?

Agentic commerce refers to AI-driven systems that can initiate and execute payments within predefined rules and authorization frameworks, based on real-time data and contextual signals.

2. Are AI agents in payments legal in India?

AI-driven payment systems can operate in India if they comply with existing RBI regulations, consent requirements, authentication norms, and data security standards. There is currently no separate regulatory category for “AI agents.”

3. How are autonomous payments different from autopay?

Autopay executes pre-authorized recurring transactions under fixed rules. Autonomous or agent-driven payments use contextual data and predefined logic to dynamically determine when and how a payment should be executed.

4. Is agentic commerce safe?

Agentic commerce can be secure when implemented with strong guardrails, audit trails, authentication controls, and clearly defined approval thresholds.