Marketplace payments are rarely as straightforward as they appear. While customers complete transactions in seconds, the movement of funds behind the scenes follows a tightly regulated structure.

In India, aggregator platforms—ranging from e-commerce marketplaces and food delivery apps to SaaS platforms and gig economy networks—handle a significant share of digital transactions. As these platforms grow, one question becomes increasingly important for founders, finance teams, and developers alike: how do you move money between customers and sellers without taking ownership of it?

The answer lies in a well-defined and regulated seller fund holding architecture. This framework enables platforms to facilitate payments while remaining compliant with financial regulations. Instead of taking custody of funds, aggregators act as orchestrators of money movement—routing transactions through bank-controlled escrow systems that ensure security, transparency, and accountability.

Understanding how this architecture works is essential for any business building or scaling a marketplace in India.

TL;DR

- Aggregators do not own seller funds; they facilitate movement through regulated systems

- Funds are held in bank-managed escrow accounts, not on the platform’s balance sheet

- RBI regulations enforce strict aggregator compliance and fund segregation

- Settlement cycles are time-bound and auditable

- API-driven infrastructure enables scalable and automated marketplace fund management

What Is Seller Fund Holding Architecture?

Seller fund holding architecture refers to the structured system through which aggregator platforms collect, route, and settle payments to sellers without taking custody or legal ownership of those funds. Instead of being held by the platform, the funds are maintained in bank-controlled escrow accounts, where they are managed on behalf of sellers until predefined settlement conditions are met.

This architecture is not just a technical design but a regulatory requirement in India under RBI guidelines. It ensures that platforms cannot misuse customer funds, enforces clear segregation of money flows, and enables transparent, time-bound payouts to sellers.

Key Components of the Architecture

A typical seller fund holding architecture consists of several interconnected layers that work together to enable compliant and efficient fund flows:

- Payment Layer: Supports customer payment methods such as UPI, cards, and net banking

- Payment Gateway / Acquiring Bank: Routes transactions and enables authorization through banking networks

- Escrow Account (Bank-Controlled): Holds funds on behalf of sellers under regulatory oversight, allowing only permitted credits and debits

- Reconciliation Engine: Matches transactions across systems, ensuring accuracy, traceability, and audit readiness

- Settlement Layer: Transfers funds to sellers after validation, based on defined settlement cycles

This architecture creates a controlled flow of funds where the platform facilitates transactions without taking custody or ownership of the money.

Why Aggregators Cannot Directly Hold Seller Funds

In India, aggregator platforms must follow a structured approach when handling customer payments. They cannot treat these funds as their own or hold them as part of their operational balances. Instead, funds are routed through controlled banking channels that ensure transparency and accountability.

When a customer makes a payment on a platform, the money is not retained within the platform’s own accounts. It is directed into a bank-managed escrow account, where it is held on behalf of the seller until the transaction is completed and settlement conditions are met.

This approach ensures that customer funds remain protected at all times, are not mixed with the platform’s operational finances, and are used only for specific purposes such as seller payouts, refunds, or chargebacks. It also creates a clear, traceable flow of money, which is essential for maintaining trust between buyers, sellers, and the platform.

Understanding Escrow Accounts in Marketplace Fund Management

An escrow account is central to the functioning of seller fund holding architecture. It acts as a bank-controlled holding mechanism where funds are temporarily maintained on behalf of sellers until predefined conditions are met.

How Escrow Works in Practice

When a customer completes a transaction, the payment is first processed through a payment gateway and an acquiring bank. Once authorized, the funds are routed into an escrow account maintained by the aggregator with its partner bank.

The platform then verifies whether transaction conditions—such as successful delivery or service completion—have been met. Based on this validation, the platform initiates the settlement process, and the bank releases funds from the escrow account to the seller.

Why Escrow Accounts Are Critical

Escrow accounts play a vital role in ensuring:

- Secure and compliant handling of funds

- Protection against misuse or unauthorized access

- Efficient management of refunds and disputes

- Transparent and traceable settlement flows

Without escrow-based structures, it would be difficult for platforms to manage funds at scale while maintaining compliance and trust.

Step-by-Step Flow of Seller Fund Holding Architecture

To better understand how this works in a real-world scenario, consider a food delivery platform handling a ₹500 order.

Step 1: Payment Initiation

The customer places an order and pays using UPI, card, or net banking.

Step 2: Payment Processing

The transaction is processed through a payment gateway and an acquiring bank, which authorizes the payment.

Step 3: Escrow Allocation

Once authorized, the funds are routed through banking settlement flows and reflected in the escrow account maintained by the platform’s partner bank.

Step 4: Transaction Mapping

The platform records and maps transaction details, including order ID, seller ID, and payment status, creating a structured record for downstream processing.

Step 5: Reconciliation and Validation

The system verifies that the payment was successful, the order was fulfilled, and there are no disputes or refund triggers. This ensures all transaction data is accurate and aligned across systems.

Step 6: Settlement

Based on predefined settlement cycles, the platform initiates the payout, and the bank releases funds from the escrow account to the seller after deducting the platform’s commission.

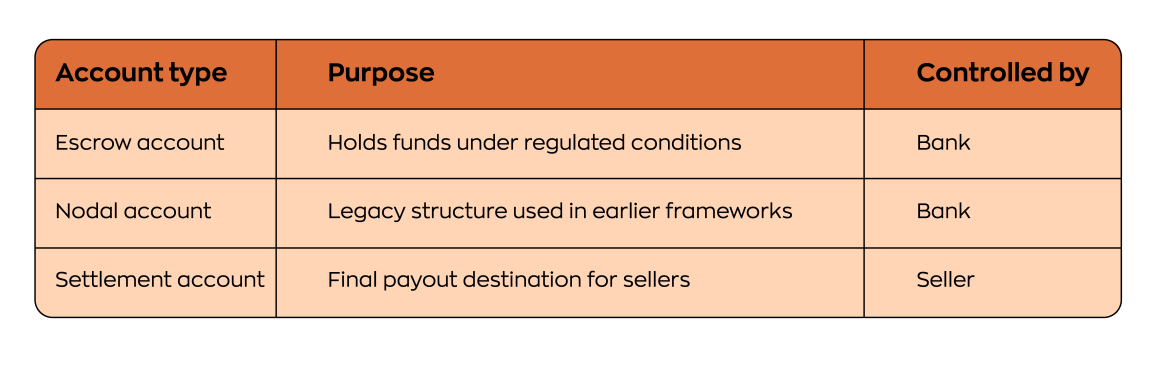

Types of Accounts in Aggregator Compliance

It is important to note that under current RBI guidelines, escrow accounts are the primary mechanism used by aggregators, while nodal accounts were more common in earlier regulatory structures.

Key Compliance Requirements for Aggregators in India

To operate responsibly and at scale, aggregator platforms must adhere to several critical compliance requirements.

1. Fund Segregation

Seller funds must always remain separate from the platform’s own funds, ensuring they are not mixed with operational balances.

2. Defined Settlement Timelines

Settlements are typically processed within defined timelines such as T+1 or T+2, depending on merchant agreements, risk checks, and operational considerations.

Merchant KYC and Onboarding

Platforms are required to perform due diligence and KYC verification before onboarding sellers and enabling payouts.

Audit Trails and Reconciliation

Platforms are expected to maintain robust audit trails and perform regular reconciliation to ensure transaction-level accuracy and traceability across systems.

Restricted Usage of Funds

Funds held in escrow can only be used for specific purposes such as seller payouts, refunds, and chargebacks, ensuring controlled and compliant fund flows.

Core Portion of Escrow Balances

A portion of escrow balances may be maintained as a “core portion” for operational stability, subject to specific conditions, including how any associated interest is handled.

Challenges in Marketplace Fund Management

- Managing funds at scale introduces significant operational complexity, even with a well-defined structure in place.

- As transaction volumes grow, platforms must handle large volumes of payments across multiple sellers, each with different settlement timelines, payout structures, and business conditions.

- Multi-party settlements become harder to manage efficiently, increasing the risk of delays or errors.

- Reconciliation becomes increasingly complex, as platforms need to match transaction data across payment gateways, banking systems, and internal records.

- Even minor mismatches can lead to payout delays, reporting inconsistencies, or compliance risks.

- Handling refunds, chargebacks, and disputes adds another layer of complexity, requiring accurate transaction reversals and clear audit trails.

- Ensuring compliance at scale—through proper fund segregation, traceability, and reporting—can become resource-intensive without the right systems in place.

- As a result, many platforms invest in automated, API-driven infrastructure to manage these challenges more effectively.

How Modern Seller Fund Holding Architecture Solves These Challenges

Modern fintech infrastructure has significantly simplified how platforms implement and manage compliant fund flows, especially as transaction volumes scale.

1. API-Driven Automation

APIs enable platforms to automate critical workflows such as payment routing, escrow allocation, and settlement processing. This reduces manual intervention, minimizes errors, and ensures consistent execution of fund flows across large transaction volumes.

2. Real-Time Visibility

Platforms gain access to real-time dashboards that provide visibility into transaction status, escrow balances, settlements, and exceptions. This helps teams quickly identify issues, track payouts, and maintain operational control.

3. Smart Reconciliation Systems

Advanced reconciliation systems automatically match transaction data across payment gateways, banking systems, and internal records. This significantly reduces mismatches and ensures accurate, audit-ready records.

4. Built-In Compliance Controls

Modern systems embed compliance into the architecture by enforcing fund segregation, restricting fund usage, and maintaining detailed audit trails. This reduces the operational burden of meeting regulatory requirements.

5. Scalable Settlement Infrastructure

Automated settlement engines allow platforms to manage payouts across multiple sellers with varying settlement cycles, ensuring timely and efficient fund distribution even at scale.

Pro Tips for Building a Strong Seller Fund Holding Architecture

- Choose banking partners that can support escrow structures and scale with transaction volumes.

- Automate reconciliation processes early to reduce errors and operational overhead.

- Define clear settlement cycles aligned with business models and risk considerations.

- Build robust refund and dispute workflows to handle reversals without impacting payouts.

- Maintain audit-ready records and transaction-level traceability at all times.

Common Mistakes to Avoid

- Mixing seller funds with platform finances leads to compliance risks.

- Delaying settlements without clear communication impacts seller trust.

- Relying on manual reconciliation processes that do not scale with volume.

- Ignoring evolving compliance requirements and regulatory expectations.

- Lacking visibility into transaction status leads to operational inefficiencies.

The Future of Aggregator Compliance in India

- Faster and more flexible settlement cycles, driven by real-time payment systems.

- Increased adoption of UPI and embedded finance across platforms.

- Greater emphasis on transparency and real-time visibility into fund flows.

- Shift toward automated, API-driven compliance and reconciliation systems.

- Deeper integration between payment infrastructure and business operations.

How Zwitch Enables Seamless Seller Fund Holding Architecture

Building and managing a compliant seller fund holding architecture involves multiple layers—from escrow handling and reconciliation to settlement and compliance workflows. Implementing and maintaining these systems in-house can quickly become complex, especially as platforms scale and transaction volumes grow.

Zwitch simplifies this by offering API-first infrastructure that helps platforms manage key components such as payment collection, escrow-based fund flows, automated reconciliation, and multi-party payouts. By reducing the complexity of payment orchestration and compliance processes, Zwitch enables businesses to streamline marketplace fund management and build a scalable, future-ready financial stack.

Explore Zwitch’s APIs to simplify your fund flows.

FAQs

1. What is the seller fund holding architecture?

Seller fund holding architecture refers to the system that allows platforms to manage and route seller payments without taking ownership of funds, typically using escrow accounts to ensure compliance, transparency, and security.

2. How do escrow accounts work in India?

Escrow accounts are bank-managed accounts where funds are held on behalf of sellers and released based on predefined conditions such as order completion, settlement timelines, or risk checks, ensuring controlled and traceable fund flows.

3. Can aggregators legally hold customer funds?

Aggregators do not hold customer funds as their own. Instead, they facilitate fund flows through bank-managed escrow accounts, ensuring that funds remain protected and are used only for permitted purposes.

4. What is the difference between escrow and nodal accounts?

Escrow accounts are the primary structure used under current RBI guidelines for managing funds, while nodal accounts were more commonly used in earlier regulatory frameworks for intermediary fund handling.